Choosing between a bank and a fintech is less about culture and more about your personal investment strategy.

- Fintechs offer high-risk, high-reward equity but require due diligence on their financial health and market position.

- Traditional banks provide stability and predictable growth but often come with slower innovation and career velocity.

Recommendation: Before accepting any offer, analyze the company’s burn rate and the true, diluted value of its equity package to make a calculated career investment.

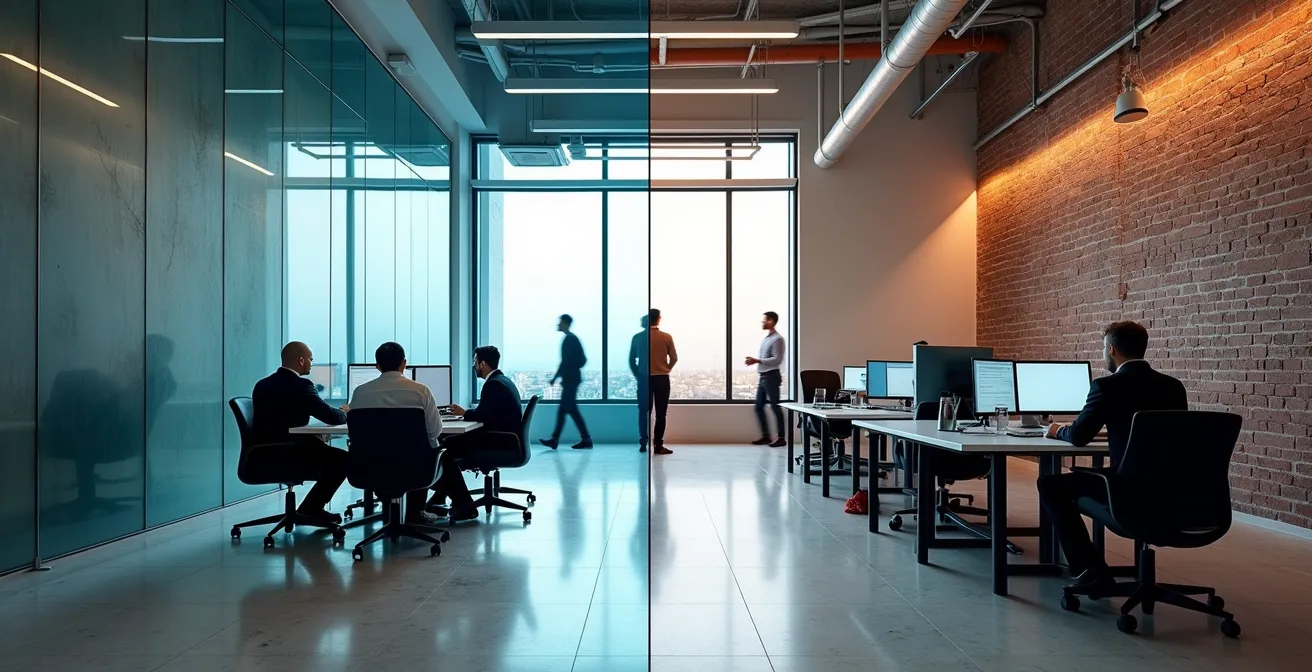

For any finance professional at a career crossroads, the dilemma is classic: the polished prestige of a traditional banking role versus the volatile excitement of a fintech startup. The common narrative frames this as a simple lifestyle choice. On one side, the perceived stability, structured career paths, and significant bonuses of legacy institutions. On the other, the promise of innovation, flat hierarchies, and a culture powered by free coffee and stock options.

But this surface-level comparison misses the point. The platitudes about beanbag chairs versus corner offices obscure the real factors that should drive your decision. What if this wasn’t just a choice between two different work environments? What if it was a sophisticated investment decision about the single most important asset you have: your career?

This guide reframes the debate entirely. We will treat your career as a portfolio and equip you with the mindset of a fintech career consultant. The goal is to move beyond cultural clichés and give you the tools to perform proper due diligence. You will learn to analyze the risk-adjusted returns of each path, scrutinize the real value of a fintech equity package, assess the operational drag of a regulated giant, and understand how to check a startup’s financial vital signs before you sign on the dotted line. By the end, you’ll be able to build a career thesis that aligns with your personal tolerance for risk and your long-term wealth-building goals.

This article provides a complete framework for analyzing your next career move, from the fine print in an offer letter to the macroeconomic signals of emerging tech hubs. Explore the sections below to build your investment case.

Summary: A Finance Professional’s Guide to Career Investment in Banking and Fintech

- Stock Options in Fintech: Lottery Ticket or Real Wealth Building?

- Agile Finance: Can You Handle Weekly Sprints in a Regulated Industry?

- KYC/AML: Why Compliance is the Hottest Skill in Fintech Right Now?

- Do You Need to Code to Be a Product Manager in Fintech?

- Burn Rate: How to Check a Fintech’s Financial Health Before Joining?

- How to Avoid Losing 4% on Every Transfer Between Your Home and Host Bank?

- Why Moving to London for Finance Jobs Might Be a Bad Idea for Juniors Right Now?

- Which Tech Hub Offers the Best Salary-to-Cost-of-Living Ratio for Developers?

Stock Options in Fintech: Lottery Ticket or Real Wealth Building?

The allure of fintech equity is powerful, often presented as a path to life-changing wealth. However, treating stock options as a guaranteed bonus is a critical error in your career investment analysis. The reality is far more complex, resembling an investment in a high-risk growth stock rather than a stable dividend-paying asset. Market fluctuations and funding rounds can dramatically alter the value of your stake before you ever see a penny. For instance, the cooling venture capital market led to a 37% decline in average equity packages for startup employees between late 2022 and early 2024, a stark reminder that paper wealth can evaporate.

The potential reward, however, remains substantial. For those who join at the right time, the upside can be immense. Early-stage employees in a successful fintech might secure 0.5% to 2% in equity, while even senior hires can command stakes of 0.1% to 0.5%. For a company that achieves a billion-dollar valuation, even a fraction of a percent represents significant wealth. The key is to assess the probability of that success. This requires shifting from a passive employee mindset to that of a discerning venture capitalist, scrutinizing the company’s valuation, funding stage, and leadership team.

Before you get dazzled by the projected numbers in an offer letter, you must conduct thorough due diligence. The questions you ask about your equity package are the most important part of your risk assessment. They reveal not only the potential value of your options but also the transparency and maturity of the company you’re considering joining.

Your Due Diligence Checklist for Equity Packages

- What percentage of the company’s fully diluted shares do my options represent?

- What was the company’s most recent 409A valuation, and when was it conducted?

- What is the vesting schedule, is there a cliff, and are there any single or double-trigger acceleration clauses for acquisitions?

- Are these Incentive Stock Options (ISOs) or Non-qualified Stock Options (NSOs), and what are the specific tax implications for me upon exercise and sale?

- What is the company’s formal policy on providing equity refresh grants to retain top performers after the initial grant has vested?

Agile Finance: Can You Handle Weekly Sprints in a Regulated Industry?

The cultural divide between traditional banking and fintech is most apparent in their operational rhythms. Banks, bound by legacy systems and immense regulatory oversight, operate on quarterly or annual cycles. Projects are meticulously planned, with layers of approval creating what can feel like ‘operational drag’. Fintech, in contrast, lives by the principles of agile methodology: weekly sprints, rapid prototyping, and a “fail fast, learn faster” mantra. This environment offers a higher ‘return on effort’, where an individual’s contribution can directly influence the product in a matter of days, not months.

This pace is not for everyone. It demands a tolerance for ambiguity, a willingness to pivot quickly, and a comfort level with continuous feedback. While a bank provides the psychological safety of established processes, a fintech thrives on challenging those very processes. The reward is a sense of ownership and direct impact that is rare in a larger, more siloed organization. As one fintech leader puts it, the difference is fundamental.

As described by the Chief Operating Officer at Starling Bank:

The key difference is mind-set – the agile organisation spends more time thinking of the customer, thinking how to run the business better and less politics, less stakeholder management and more getting the job done.

– Chief Operating Officer, Starling Bank

Choosing between these models is an investment in a work style. The ‘stable, predictable returns’ of a bank’s structure suit those who thrive on clarity and long-term planning. The ‘high-growth, high-volatility’ environment of a fintech is for those who are willing to trade procedural certainty for speed and influence. Your decision should be based on a frank assessment of which environment will best compound your skills and job satisfaction over time.

KYC/AML: Why Compliance is the Hottest Skill in Fintech Right Now?

In the early days of fintech, the spotlight was on disruptive engineers and visionary product managers. Today, the most sought-after and highly compensated roles are often in a less glamorous but far more critical field: compliance. As fintech companies mature from scrappy startups to regulated financial institutions, their very survival depends on robust Know Your Customer (KYC) and Anti-Money Laundering (AML) frameworks. A single compliance failure can result in crippling fines, loss of licenses, and reputational ruin, making expertise in this area a board-level concern.

This has created a massive talent squeeze. There is soaring demand for Chief Risk Officers and compliance chiefs, with a supply of qualified candidates that has not kept pace. From an investment perspective, this makes compliance skills a severely ‘undervalued asset’ with enormous growth potential. Recruiters report that fintechs are aggressively bidding for top compliance talent, with compensation packages now rivaling those of Chief Technology Officers. The reason is simple: a strong compliance function is no longer a cost center but a competitive advantage, enabling a fintech to onboard larger enterprise clients and expand into new, more complex markets.

For a finance professional with a background in regulatory affairs, this is a golden opportunity. While a similar role in a traditional bank offers a stable, well-defined career path, the same skills applied in a fintech context offer a faster track to a leadership position with strategic influence. You are not just checking boxes; you are building the very foundation of trust that allows the company to scale. The ability to navigate complex regulatory landscapes while maintaining the agility of a tech company is the new power skill in finance.

Do You Need to Code to Be a Product Manager in Fintech?

A common misconception is that a successful career in fintech, particularly in product management, requires a background in software engineering. While technical literacy is essential, the belief that you must be able to write code is largely a myth. The most effective fintech Product Managers (PMs) are often translators, bridging the worlds of finance, technology, and customer experience. Their core value lies not in building the product themselves, but in deeply understanding the financial problem to be solved and articulating the solution so clearly that engineers can build it flawlessly.

The financial rewards for those who master this skill are significant. In major hubs, experienced fintech product managers can earn over $250,000 annually. However, this compensation is tied to a specific set of non-coding skills. The best PMs possess a unique combination of systems thinking and technical empathy. They may not write SQL, but they understand database architecture. They don’t configure APIs, but they can design intricate, API-level user flows. Their expertise is in the logic of finance, not the syntax of Python.

For a finance professional looking to transition, the key is to build a portfolio of these adjacent skills. Instead of learning to code, focus on mastering the underlying mechanics of financial technology. Key areas to develop include:

- Systems Thinking: Deconstruct how payment rails, ledger systems, and third-party APIs interact to deliver a seamless user experience.

- Technical Empathy: Learn to “speak engineer” by understanding product architecture and the trade-offs involved in technical decisions.

- Regulatory Expertise: Build deep knowledge of the regulatory frameworks (e.g., PCI-DSS, GDPR) that directly impact product features and data handling.

- Data Analytics: Develop a strong command of data analysis to inform product decisions, even if you are not the one running the queries.

Burn Rate: How to Check a Fintech’s Financial Health Before Joining?

Accepting a job at a fintech without investigating its financial health is like investing in a stock without reading its quarterly report. The most critical metric to understand is the net burn rate: the speed at which the company is spending its venture capital funding. This single number determines the company’s ‘runway’—the number of months it can survive before it needs to raise more money or become profitable. A high burn rate coupled with a short runway is a major red flag for job security, no matter how exciting the product is.

So how do you, as a candidate, perform this due diligence? While you won’t get access to the full financial statements, you can look for intelligent proxies. One of the most telling indicators is headcount relative to funding stage. In the current market, investors are rewarding efficiency. Leaner teams are a sign of disciplined capital management. For example, recent data shows that startups raising seed funding in the first half of 2024 had an average of 5.3 employees, down from 6.9 in 2021. A startup that is over-hiring relative to its peers may be burning through cash too quickly.

During the interview process, you are well within your rights to ask pointed questions. Frame your inquiry professionally, as a sign of your strategic thinking. Ask questions like, “Could you share how the company is thinking about its runway and path to profitability?” or “How has the company’s hiring plan been adjusted to reflect the current funding environment?” The response—whether it’s transparent and confident or vague and evasive—will tell you everything you need to know about the company’s financial stability and leadership’s grasp on the business.

How to Avoid Losing 4% on Every Transfer Between Your Home and Host Bank?

The difference between a traditional bank and a fintech is not just a matter of culture; it’s deeply embedded in their technological foundations, with direct consequences for the end user. A clear example of this is the cost and speed of international money transfers. A finance professional working abroad might lose up to 4% of their money in hidden fees and poor exchange rates when moving funds through legacy banking systems. This ‘leakage’ is a direct result of the ‘operational drag’ inherent in institutions built on decades-old infrastructure that requires manual processes and multiple intermediaries.

Fintechs, in contrast, were built to solve these inefficiencies. They approached the problem from a digital-first perspective, leveraging modern technology to create a more streamlined and cost-effective solution. As one industry analysis notes, this is a core differentiator:

Fintechs are born digital enterprises, with product development taking place on cloud platforms using AI and APIs to render truly seamless experiences.

– Industry Analysis, GTech Middle East Financial Report

This fundamental difference in architecture—legacy systems versus a ‘born digital’ stack—manifests across every aspect of the customer experience. From transaction speed to fee structures, the two models offer vastly different value propositions. The following table illustrates the practical impact of these divergent philosophies.

| Aspect | Traditional Banking | Fintech |

|---|---|---|

| Transaction Speed | Days for processing | Real-time or minutes |

| Fee Structure | Multiple fees (maintenance, ATM, overdraft) | Low-cost or fee-free |

| Innovation | Legacy systems, slower adoption | AI-powered tools, rapid innovation |

| Customer Service | In-person branches, phone support | 24/7 chatbots, app-based support |

From a career perspective, this highlights the core trade-off. Working at a bank means operating within a proven but rigid system. Working at a fintech means building and refining a system designed to dismantle that rigidity, with all the associated risks and rewards.

Why Moving to London for Finance Jobs Might Be a Bad Idea for Juniors Right Now?

For decades, London has been the undisputed heavyweight champion of European finance, a ‘blue-chip’ investment for any ambitious junior professional. However, a smart investment thesis requires looking beyond past performance and analyzing current market conditions. Right now, several factors suggest that moving to London for an entry-level finance role may not offer the best risk-adjusted return. While salaries appear high, with London finance entry positions typically starting from £45,000 to £60,000, they are severely eroded by one of the highest costs of living in the world.

More importantly, the competitive landscape is shifting. Post-Brexit, other European hubs are aggressively courting finance and tech talent, creating compelling alternative ‘markets’ for your career capital. Amsterdam, for instance, has quietly overtaken London as Europe’s top share trading center. The city offers competitive salaries that stretch further due to a lower cost of living, combined with a burgeoning fintech ecosystem. Organizations like Holland Fintech and Amsterdam Fintech Week provide powerful networking opportunities that may be more accessible to junior professionals than the saturated London scene.

This doesn’t mean London is a ‘bad’ market, but it may be ‘overvalued’ for those just starting out. The intense competition for a limited number of junior roles can lead to burnout, while the high cost of living can make it difficult to build savings. From a portfolio perspective, concentrating all your career capital in a single, high-cost, high-competition market is a risky strategy. A more diversified approach, considering emerging hubs like Amsterdam, Dublin, or Berlin, might offer a better balance of opportunity, salary, and quality of life for a junior professional’s ‘investment horizon’.

Key takeaways

- Equity is not guaranteed wealth; perform due diligence with specific, targeted questions about dilution and valuation before accepting an offer.

- A fintech’s financial health, measured by its burn rate and runway, is a critical indicator of job security and should be assessed during the interview process.

- High-demand skills like regulatory compliance (KYC/AML) have become a strategic advantage, yielding compensation packages that can rival senior technology roles.

- Geographic arbitrage is key; established hubs like London may be ‘overvalued’ for juniors, while emerging centers offer better salary-to-cost-of-living ratios.

Which Tech Hub Offers the Best Salary-to-Cost-of-Living Ratio for Developers?

The final component of your career investment thesis is geographic analysis. A high salary is meaningless if it’s consumed by an exorbitant cost of living. To truly measure your potential return, you must analyze the salary-to-cost-of-living ratio offered by different tech hubs. This calculation reveals your true earning power and ability to build wealth. While cities like London and Zurich offer some of the highest absolute salaries, they often fall short when adjusted for expenses.

Emerging and established fintech hubs across Europe are now competing fiercely on this very metric. The Netherlands, for example, presents a compelling case. Not only do finance professionals in the Netherlands earn between €50,000 to €140,000 annually, but skilled expats can also benefit from the ‘30% ruling’, a significant tax advantage that dramatically increases disposable income. This kind of structural benefit is a crucial variable in your analysis. It’s a ‘market inefficiency’ you can leverage to your advantage.

When comparing opportunities, it’s essential to look beyond the headline salary and create a comprehensive financial picture for each location. Consider tax implications, average rent, transportation costs, and other key benefits that may be offered. A lower salary in a city with excellent public transport, affordable housing, and unique tax incentives may provide a far greater long-term return than a top-tier salary in a hyper-expensive metropolis.

| Location | Salary Range | Key Benefits |

|---|---|---|

| London | £50,000-£100,000 | Stock options, learning budgets |

| DACH Region | 5-10% higher than UK | AI/blockchain focus |

| Amsterdam | €40,000-€90,000 | AI/ML emphasis, embedded finance |

| Dublin | €50,000-€100,000 | Low corporate tax, fintech density |

Ultimately, the choice between traditional banking and fintech is not a binary one of ‘safe’ versus ‘risky’. It is a spectrum of investment opportunities. By applying a rigorous, data-driven framework, you can move past the cultural stereotypes and identify the path that offers the best risk-adjusted return for your unique skills, ambitions, and financial goals. To make your next career move a calculated investment, not a gamble, start by applying this due diligence framework to your current opportunities.